All Categories

Featured

Table of Contents

IUL contracts secure against losses while offering some equity threat premium. Individual retirement accounts and 401(k)s do not supply the very same disadvantage security, though there is no cap on returns. IULs tend to have actually have complicated terms and greater charges. High-net-worth people seeking to decrease their tax obligation concern for retirement may gain from purchasing an IUL.Some investors are better off acquiring term insurance coverage while optimizing their retired life plan contributions, rather than buying IULs.

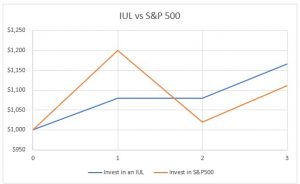

If the underlying supply market index goes up in a given year, owners will certainly see their account rise by a symmetrical quantity. Life insurance firms utilize a formula for determining just how much to attribute your cash money balance. While that formula is tied to the efficiency of an index, the amount of the credit score is usually mosting likely to be much less.

Employers often provide coordinating contributions to 401(k)s as a benefit. With an indexed universal life policy, there is a cap on the amount of gains, which can limit your account's development. These caps have yearly top limits on account credit scores. If an index like the S&P 500 boosts 12%, your gain can be a fraction of that quantity.

Transamerica Iul Calculator

Irrevocable life insurance counts on have actually long been a prominent tax sanctuary for such people. If you fall right into this category, think about speaking to a fee-only monetary advisor to discuss whether buying irreversible insurance policy fits your general strategy. For several financiers, though, it might be much better to max out on contributions to tax-advantaged retired life accounts, specifically if there are contribution matches from an employer.

Some plans have an assured price of return. One of the crucial features of indexed global life (IUL) is that it offers a tax-free circulations.

Asset and tax obligation diversity within a profile is enhanced. Pick from these products:: Supplies long-lasting growth and earnings. Suitable for ages 35-55.: Offers flexible insurance coverage with modest money worth in years 15-30. Suitable for ages 35-65. Some points customers ought to think about: For the fatality benefit, life insurance policy items bill costs such as death and cost danger costs and surrender charges.

Retired life preparation is important to preserving monetary security and preserving a specific requirement of living. of all Americans are fretted about "preserving a comfy requirement of living in retired life," according to a 2012 study by Americans for Secure Retired Life. Based on current data, this bulk of Americans are warranted in their issue.

Department of Labor estimates that an individual will need to keep their present criterion of living as soon as they start retired life. Furthermore, one-third of united state property owners, in between the ages of 30 and 59, will certainly not have the ability to keep their requirement of living after retirement, also if they delay their retired life till age 70, according to a 2012 study by the Fringe benefit Research Study Institute.

Indexed Universal Life (Iul) Vs. 401(k): An In-depth Retirement Comparison

In 2010 greater than 80 percent of those between age 50 and 61 held financial debt, according to the Social Safety And Security Administration (SSA). The ordinary financial debt quantity among this age group was even more than $150,000. In the same year those aged 75 and older held an average debt of $27,409. Amazingly, that figure had even more than increased since 2007 when the typical financial debt was $13,665, according to the Employee Benefit Research Study Institute (EBRI).

56 percent of American retired people still had superior debts when they retired in 2012, according to a study by CESI Financial debt Solutions. The Roth Individual Retirement Account and Policy are both devices that can be utilized to build substantial retired life cost savings.

These monetary devices are similar in that they profit policyholders who desire to generate cost savings at a lower tax obligation rate than they may experience in the future. Nonetheless, make each extra appealing for people with varying demands. Identifying which is better for you depends on your individual scenario. In either instance, the policy grows based on the rate of interest, or returns, credited to the account.

That makes Roth IRAs suitable cost savings vehicles for young, lower-income employees who live in a reduced tax obligation brace and that will certainly gain from years of tax-free, compounded development. Since there are no minimum required payments, a Roth individual retirement account provides investors regulate over their personal objectives and run the risk of tolerance. Additionally, there are no minimum called for circulations at any age throughout the life of the policy.

a 401k for employees and employers. To compare ULI and 401K strategies, take a minute to comprehend the essentials of both items: A 401(k) allows employees make tax-deductible payments and enjoy tax-deferred growth. Some employers will match part of the staff member's contributions (chicago iul). When staff members retire, they generally pay tax obligations on withdrawals as common revenue.

Can You Maximize Your Retirement By Using Both Iul And 401(k)?

Like various other long-term life plans, a ULI policy likewise allots component of the costs to a money account. Given that these are fixed-index plans, unlike variable life, the plan will also have actually a guaranteed minimum, so the money in the money account will certainly not reduce if the index decreases.

Plan proprietors will likewise tax-deferred gains within their cash money account. They may likewise appreciate such various other monetary and tax obligation benefits as the capacity to obtain versus their tax obligation account instead of withdrawing funds. In that means, universal life insurance policy can work as both life insurance and a growing possession. Explore some highlights of the benefits that universal life insurance policy can supply: Universal life insurance plans don't impose limitations on the dimension of policies, so they might supply a method for employees to conserve even more if they have currently maxed out the IRS restrictions for various other tax-advantaged financial items.

The IUL is much better than a 401(k) or an individual retirement account when it involves conserving for retirement. With his almost 50 years of experience as a financial planner and retired life planning specialist, Doug Andrew can show you precisely why this is the instance. Not just will Doug explains why an Indexed Universal Life insurance agreement is the better car, but also you can likewise learn how to enhance possessions, reduce tax obligations and to empower your authentic wealth on Doug's 3 Dimensional Wealth YouTube channel. Why is tax-deferred build-up much less desirable than tax-free build-up? Discover how postponing those taxes to a future time is taking a horrible danger with your savings.

%20Vs.%20Indexed%20Universal%20Life%20(Iul)%20Insurance%3A%20Pros%20And%20Cons){kind=link}

Latest Posts

Equity Indexed Insurance

Is Indexed Universal Life A Good Investment

Iul Retirement Pros And Cons